Business valuation: How investors determine the value of your business

Read time: 4 mins

Highlights (click to read)

When you enter into a business valuation discussion with investors, make sure that you understand the key terms.

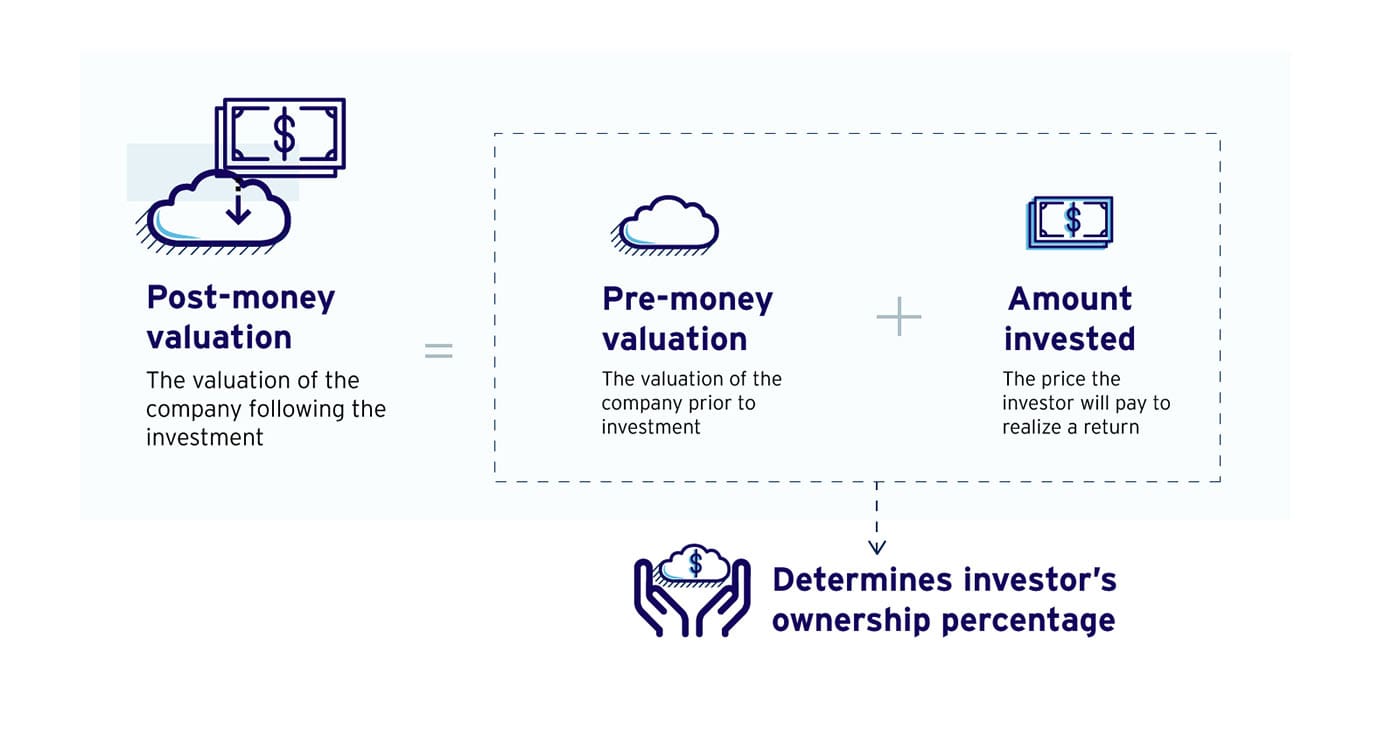

The pre-money valuation and the amount invested determine the investor’s ownership percentage following the investment.

The pre-money valuation and the amount invested determine the investor’s ownership percentage following the investment.For example, if the pre-money valuation is $4 million and the investment is $1 million, then the percentage ownership is calculated as:

Equity owned by investor = Amount invested ÷ (Agreed pre-money valuation + Amount invested)

Equity percentage owned by investor = $1M/($4M + $1M) = 20%

Post-money valuation = Pre-money valuation + Amount invested

= $4M + $1M = $5M

The pre- and post-money valuations cannot be analyzed in isolation when evaluating the financial merits of a proposed valuation. You should also consider other factors—such as liquidation preferences and dividends—to determine if it truly is a good deal.

Methods of business valuation

Most traditional corporate finance valuation methodologies do not work well for early-stage companies. Discounted cash flow (DCF) is an appropriate methodology for established companies that have a history of revenues and costs. Assumptions about market growth rates, market share, gross margins and other variables can be made to generate scenarios that will establish a valuation range. These assumptions cannot be accurately approximated for an early-stage company, which makes the results questionable.

Price/earnings (P/E) multiple is not appropriate, since most early-stage businesses are losing money. Price/sales (P/S) may be used if a company has generated some sales for a few years.

Most venture capital funds (VCs) investing in early-stage companies will use two valuation methodologies to establish the price they will pay for an investment:

- Recent comparable financings: The VC will identify similar companies, in sector and stage, as the investment opportunity. Several databases—including VentureSource, Venture Wire and VentureXpert —might provide information that establishes a valuation range for comparable companies. However, transactions that are more than two years old are not considered market. Although some information may not be public, many entrepreneurs and VCs know through word of mouth what the recent valuations have been for comparable companies.

- Potential value at exit: VCs and other investors have a good sense of a company’s exit value. The value can be based either on recent merger and acquisition (M&A) transactions in the sector or the valuation of similar public companies. Most early-stage investors look for 10 to 20 times the return on their investment (later-stage investors tend to look for 3 to 5 times the return) within two to five years.

-

- For example, assume an exit valuation of $100 million and the VC owns 20% of the company at the time of the exit. The VC would earn $20 million on their investment at exit. If the VC invested $1 million into the company, they would make 20 times their investment. If the VC owned 20% for a $1 million investment, then the post-money valuation of the company at the time of the initial investment was $5 million. As you can see, investors use the post-money valuation to estimate the price an investment must command when they exit or sell the company.

Investors will use these methodologies to set a valuation range. They will have a maximum valuation based on their view of the future valuation and the perceived competitiveness for the deal, but will try to keep the price they pay closer to the lower part of the range.

How to maximize your valuation

- Make a good case. Show the investor why there is huge potential exit value for your company.

- Maximize the potential exit valuation by removing any doubt or obstacle that the investor perceives as limiting the upside valuation. For example, if you have gaps in your management team, then identify the people that would join the team after the funding is secured.

- Do your homework. Understand the valuations of other companies at slightly later stages. Identify and understand the gaps (technical or commercial) between your business and theirs. Then, focus your company’s business plan on closing these gaps.

- Find an investment competitor. If there is competition for your deal, an investor will be more likely to give you a higher valuation. However, investors may speak to each other, so do not “play that card” if the competition does not exist.

Business valuation know-how

Remember the following when going through the business valuation process with an investor:

- When you are first given a valuation, ask for a higher valuation. Pushing back demonstrates that you’re confident in your business and a good negotiator. Of course, when pushing back, provide evidence and arguments as to why the valuation should be higher. According to Guy Kawasaki’sThe Art of the Start, ask for a valuation that is 25% higher than the first offer.

- Take the money and get to work if the valuation is reasonable. In most cases, businesses either make more money than you dreamed or they do not work at all. Neither the valuation nor the investor’s specific percentage will significantly affect the company’s ultimate success.

- Talk to your advisors, board members, consultants and other industry players to determine if the deal you’re getting reflects current valuations.

- Consider taking a lower valuation from the “better” investor, if you think that one investor brings more to the table than another.

Summary: If you’re entering a business valuation discussion with investors, do your homework (e.g., understanding key terms and how VCs calculate the value for early-stage companies) and get professional help in this matter by talking to an experienced advisor.

Read next: Understanding the term sheet